Fundraising 101: Term Sheets

For many founders, receiving a term sheet can be an exhilarating accomplishment. It serves as evidence of your fundraising skill, a (near) end to what can be a grueling few months, a physical manifestation of the market’s belief in your vision and (typically) a much needed cash infusion for your business. But receiving a term sheet can also be intimidating and nerve-racking, especially for first time founders that have never negotiated a financing before.

Over the years I have reviewed hundreds of term sheets and supported founders through their negotiations. Seeing that many Seed offers provides a clear view of what market norms are and aren’t. This post breaks down the lessons I’ve shared with founder colleagues and talks I’ve delivered to cohorts at Entrepreneur First. This should arm any founder with the confidence of knowing what they can and can’t push back on with prospective investors. After all, the key to effective negotiation is preparation.

Note: This post provides a high-level summary of major terms and norms. For serious reading, I must recommend the de facto bible for this topic: Venture Deals.

What is a Term Sheet?

A “term sheet” is a non-binding, typically three page, document that outlines the major terms and conditions for which an investment will be made. Because term sheets set the rules of the investment, they are only given by a “lead investor”. A lead Investor is a major investor that initiates deal, contributes a significant portion of the financing and represents the interests of other investors in the round.

It’s not a contract and carries no legal leverage. It's a mutual agreement to reach a transaction and both parties have committed to doing this in good faith. Getting a term sheet is an exciting time, but the time to celebrate is when the money is in your account.

Within venture financings, there are a number of special terms/clauses that most first time founders will be very unfamiliar with. Some of these terms you will always need to negotiate, some terms never should be and some depend on the round and your negotiating leverage. I’ve structured the rest of this post in those three groupings.

Always Negotiate

The most important element of any term sheet is the price of the financing. This is inherently unique to each deal because every Seed stage company is unique to itself (i.e. there is no “standard” valuation for a company). Valuation, raised capital and allocation (who invests) underpins the market nature of private company financing and Seed is extremely subjective so proper fundraising process is critical.

Valuation: The bid price of the company which sets the price per share and effective dilution in the round. This price is also known as the “pre-money valuation” (i.e. value of the company prior to any new capital). There are two basic equations you need to know regarding valuation:

Pre-money + Capital Raised = Post-money

Capital Raised / Post-money = New Dilution

There are three primary guidelines regarding dilution:

Most founders give away 22% - 27% of the company at Seed

A team should never give away more than 30% in a Seed

Founders + Employees (ESOP) should own >/=50% before Series A

Allocation: The final investment amounts each investor will be granted in the round. This only affects competitive rounds but is very common for the best deals. The optimal mix is completely subjective to the given deal. Previous thoughts here.

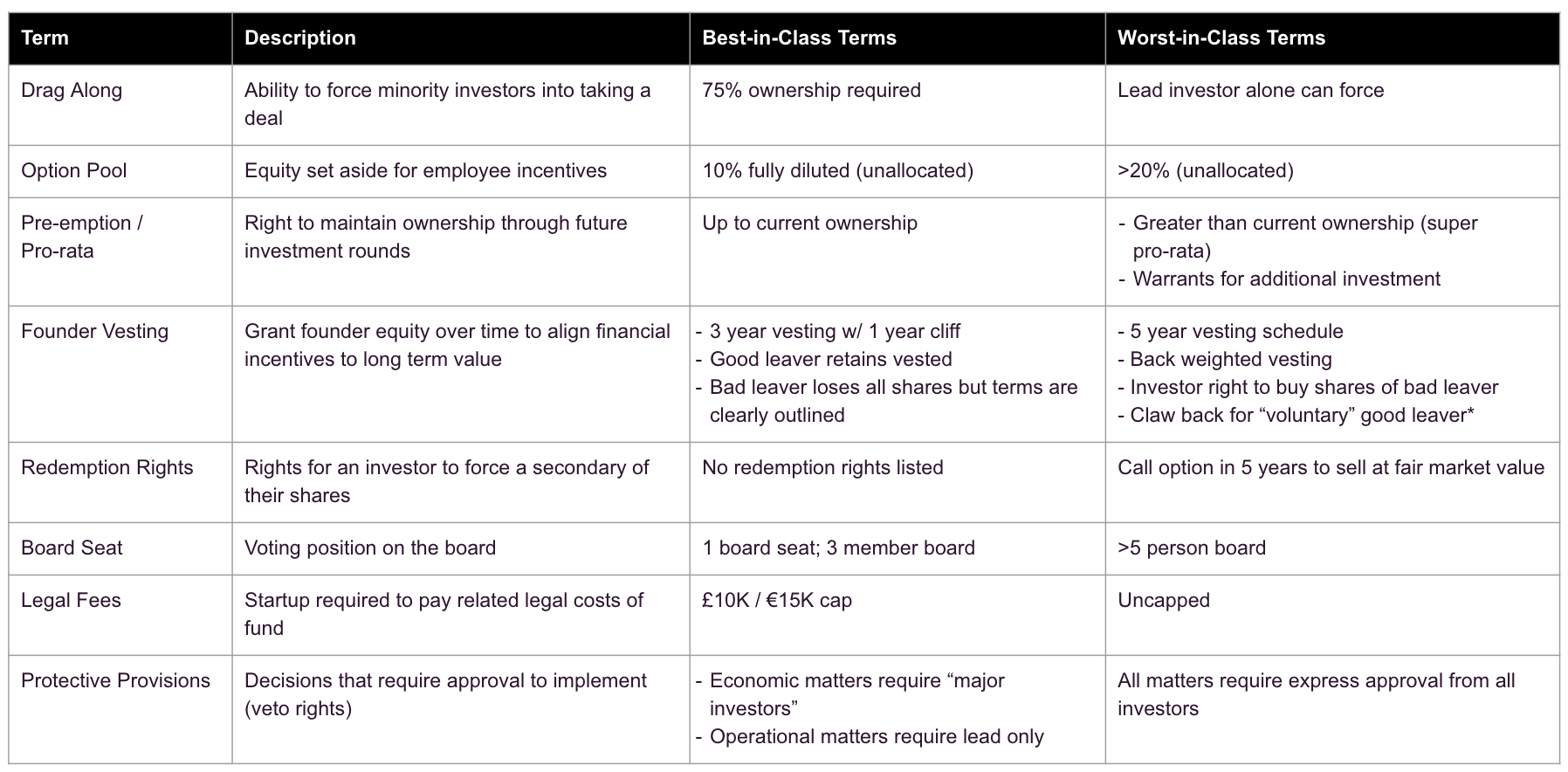

Never Negotiate

To keep this post somewhat short I threw the major terms in a table. In addition you’ll find a quick description, what you should expect (best-in-class) and some of the worst I’ve seen in market. With these terms you really shouldn’t budge and should feel comfortable pushing for "best-in-class”. If you do find yourself staring at a term sheet with out of market terms a conversation is usually all that’s needed. Most investors don’t want to be seen as predatory or outdated in their thinking and are usually quick to adjust. The majority of time I’ve seen out of market Seed terms, it’s due to the firm lifting a growth stage template.

Sometimes Negotiate

Again I’ve provided a table for easier reading. There terms are less binary so I’ve listed my view of what’s best-in-class and worst-in-class. Ideally you should negotiate yourself somewhere in between. I should also make a few clarifying notes:

My experience is heavily indexed towards UK deals. In less competitive markets you may see slightly different norms. For example, in France it’s much more common to have a 5 year call option in Redemption rights even in a Seed deal.

There are exceptions to any rule and Seed negotiations are no different. If you are negotiating a co-lead deal with two venture funds it’s expected that you’ll have both funds sit on your board. If you have a complex legal situation your fee cap is going to be higher.

*The devil is in the details here. If a clawback allows founders/management to buy back the shares from the exiting founder than it’s fine. What you want to avoid is a situation where investors benefit through perverse incentives.

With any luck your negotiation will be short lived and only focused on big economic matters like price. But a little preparation never hurt. My biggest piece of advice is to optimize for the quality of investor you take on your cap table, but that’s another post entirely.

Special thanks to Gabriel Matuschka and Jon Folland for helping write this post. And Alex Flamant for pointing out my typos.